Divorce, Debt, and YNAB: How I Found Financial Stability

Divorce is never easy.

It’s not just the emotional toll that can be overwhelming but also the financial aspect, especially when you and your partner are already in debt. For me, the thought of separating my finances from my ex-husband seemed insurmountable.

We were in such a deep financial hole, mostly due to credit card debt, that the idea of being able to afford a divorce felt impossible. But with determination, a plan, and the right tools, I was able to climb out of that financial hole and establish a stable financial footing.

One of the most essential tools in that journey was YNAB.

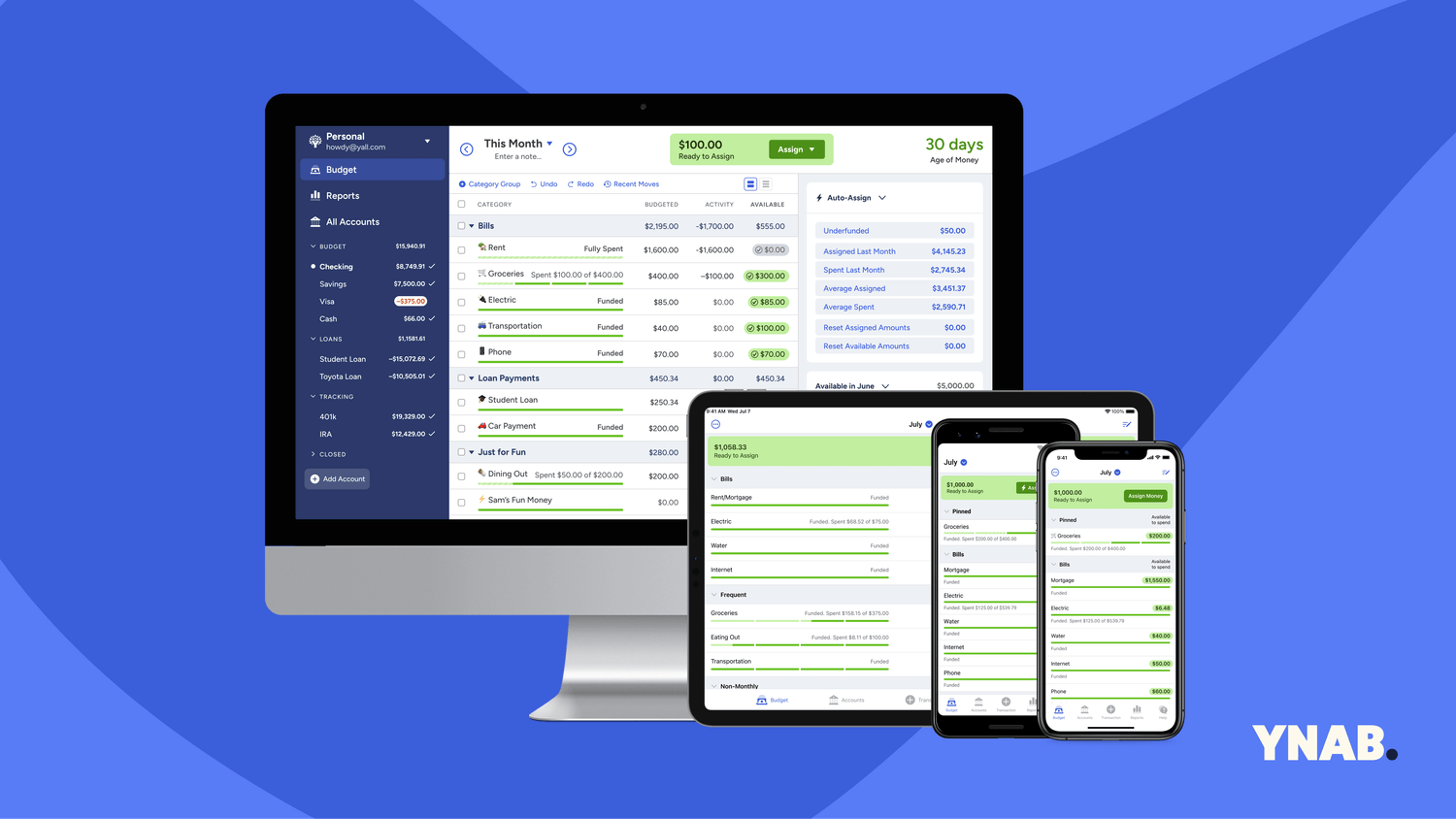

What is YNAB?

YNAB stands for "You Need A Budget," and let me tell you—I certainly did! YNAB is a budgeting app designed to help people gain control over their finances, pay off debt, and save for the future.

The YNAB budget app operates on a set of straightforward principles that are easy to follow and apply. But beyond the practical steps, it encourages a mindset shift that makes you think about money differently.

Using YNAB during my divorce was a game-changer. Not only did it allow me to track every dollar, but it also gave me a much-needed sense of control during a chaotic time. Here’s how I used YNAB to turn my finances around, even as I was going through one of the most challenging times of my life.

Getting Started: Understanding Where Our Money Was Going

When my ex-husband and I decided to part ways, we had to get brutally honest about our financial situation. We were in debt, with most of it on high-interest credit cards, and we were living paycheck to paycheck. YNAB provided me with the tools to take a deep dive into our finances, so I could understand exactly where every dollar was going.

With the YNAB budget app, I was able to track every transaction in real time. The app allowed me to see where we were overspending and which expenses could be minimized.

YNAB also helped me set up custom budget categories, so I could organize our spending in a way that made sense for us. I customized categories for things like groceries, gas, and utilities, as well as for debt repayment, which quickly became my top priority.

Give Every Dollar a Job

One of YNAB’s core principles is to "Give Every Dollar a Job." This means assigning every dollar a specific purpose, whether it’s for groceries, utilities, debt repayment, or savings. By following this principle, I was able to allocate money to essential categories without wasting it on unnecessary expenses.

At a time when I felt like I had very little control over my life, giving every dollar a job gave me a renewed sense of purpose and clarity. I knew exactly where my money was going, and I could prioritize my spending according to what mattered most to me.

For example, I allocated a significant portion of our income towards debt repayment, so we could get out from under the weight of credit card interest.

Developing a Debt Repayment Plan

One of my biggest challenges was tackling the mountain of credit card debt we had accumulated over the years. YNAB allowed me to set up a custom category for each credit card, which helped me stay organized and track our progress.

I used the debt snowball method—paying off the smallest debt first and then moving on to the next one. This method gave me quick wins, which helped me stay motivated during the long journey of debt repayment.

With YNAB, I could easily categorize our credit card payments and track how much we owed. Seeing our debt numbers go down every month was incredibly empowering.

Importantly, we stopped using our credit cards entirely during this period and switched to a cash-only approach for all other spending. This meant that every dollar I saved was going towards reducing our debt rather than accruing more.

Tracking Progress with YNAB’s Import Transactions Feature

One of the standout features of YNAB is its ability to import transactions directly from your bank. Our local credit union didn’t integrate directly with YNAB, but I could still download transactions from my bank account and upload them to my YNAB budget.

This small step made a huge difference, as it allowed me to monitor my finances in real-time without the hassle of manually inputting every transaction.

Before YNAB, I was keeping track of our budget using pencil and paper and a bulky binder. This method was incredibly time-consuming and often inaccurate.

By switching to YNAB, I was able to cut my budgeting time in half, and the accuracy of my budget skyrocketed. I could see exactly where we stood financially, down to the last cent.

Relying on Budget Categories Instead of Bank Balances

One of the most important mindset shifts YNAB teaches is to stop relying on your bank balance as a measure of what you can afford. Instead, you rely on your YNAB budget categories.

Before YNAB, I would look at my bank balance and assume I could spend what was there, which often led to overdrafts and misallocated funds.

With YNAB, I knew exactly how much money was available in each category, whether it was for groceries, gas, or debt payments. This approach helped me make more intentional spending decisions, as I could see at a glance how much I had left to spend in each area.

YNAB’s mobile app also allowed me to check my budget categories in real time, so I could make informed decisions while out and about.

Fresh Start with YNAB

During the budgeting process, mistakes were inevitable, especially as I learned the ropes of YNAB. Fortunately, YNAB offers a Fresh Start feature that lets you reset your budget without losing your historical data.

A fresh start doesn’t erase your budget categories or targets—it simply allows you to start over with your current balances and continue tracking from there. Your previous budget is archived, so you don’t lose any of your transactions.

For me, this was incredibly useful. If I made an error I didn’t have to worry about starting my budget from scratch. Instead, I could hit the Fresh Start button, keep all my custom categories, and begin anew with updated balances. This feature helped me stay on track and avoid the discouragement that often comes from small budgeting missteps.

Breaking Free from the Paycheck-to-Paycheck Cycle

One of the most significant benefits I gained from YNAB was breaking free from the paycheck-to-paycheck cycle. YNAB has a feature that tells you the "age of your money"—a metric that shows how long each dollar has been in your budget. The higher the age, the less reliant you are on immediate income to cover expenses.

By following YNAB’s budgeting principles, I was able to increase the age of my money significantly. I wasn’t just paying off debt; I was building a financial cushion that gave me a sense of security.

This cushion eventually turned into a healthy emergency fund. For the first time in years, I felt a sense of financial stability.

Building an Emergency Fund and Starting to Invest

Once I had paid off our credit card debt, I turned my focus towards saving and investing. YNAB made it easy to create budget categories for these new goals. I set aside money for an emergency fund and a small investment portfolio.

After years of living paycheck to paycheck, having extra cash flow to invest in my future was incredibly empowering.

Planning for Recurring Expenses, Like the YNAB Yearly Cost

One small but essential lesson YNAB taught me was to budget for annual expenses. YNAB has a yearly cost of $109, which I’ve found to be worth every penny. Instead of scrambling to pay this fee all at once, I created a YNAB category and set aside a little over $9 per month.

This way, when the yearly cost came due, I already had the funds set aside. This small planning habit extended to other annual expenses, reducing financial surprises and allowing me to stay in control of my budget.

YNAB Walkthrough

In the video below, you can watch me walk through the main features and benefits of YNAB during one of my weekly Women's Membership Program meetings.

Accessing the YNAB Discount

If you’re considering giving YNAB a try, as a Certified YNAB Coach, I can help you get a YNAB discount of two months free.

As a CFEI, I’ve found YNAB to be an invaluable tool, and I’d love for you to experience its benefits as well. If you choose to work with me, you’ll have access to this YNAB discount, giving you a risk-free opportunity to see if YNAB fits your budgeting needs.

Moving Forward with Confidence

Today, I have a healthy emergency fund, invest for my future, and am on my way to achieving my long-term financial goals. Looking back, I’m incredibly grateful for the role YNAB played in helping me through one of the most challenging periods of my life. Divorce is never easy, and the financial hurdles can be overwhelming, but YNAB provided me with the structure and clarity I needed to regain control.

Final Thoughts

If you’re in a challenging financial situation or just want to take control of your money, I highly recommend giving YNAB a try. It’s more than just a budgeting tool—it’s a way to change your relationship with money for the better.

Whether you’re dealing with debt, saving for a major goal, or simply trying to stop living paycheck to paycheck, YNAB can help you get there.

For those considering YNAB, remember that the journey to financial freedom starts with a single step: understanding where your money is going and creating a plan for it. YNAB can be that first step toward a healthier, more intentional financial life.

And if you’re ready to take that step, don’t hesitate to reach out for guidance and a chance to access the YNAB discount. I would love the opportunity to help you build a brighter financial future.

Copyright © 2024 AJC Publications and Real Talk Finance